Coldwell Banker

2023 Real Estate Market Report

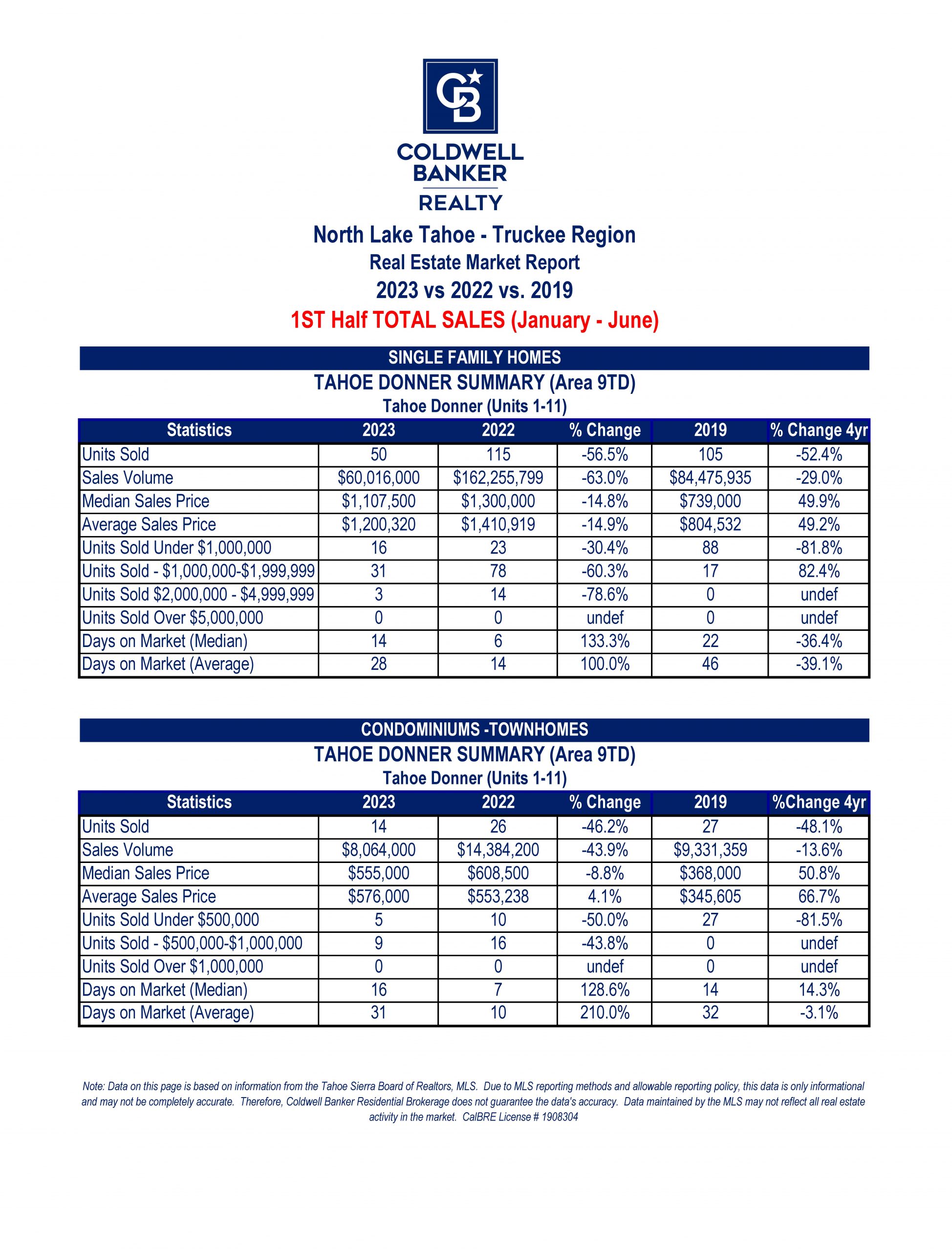

North Lake Tahoe -Truckee

Residential Properties – Single Family Homes and Condominiums

Activity January- July 2023

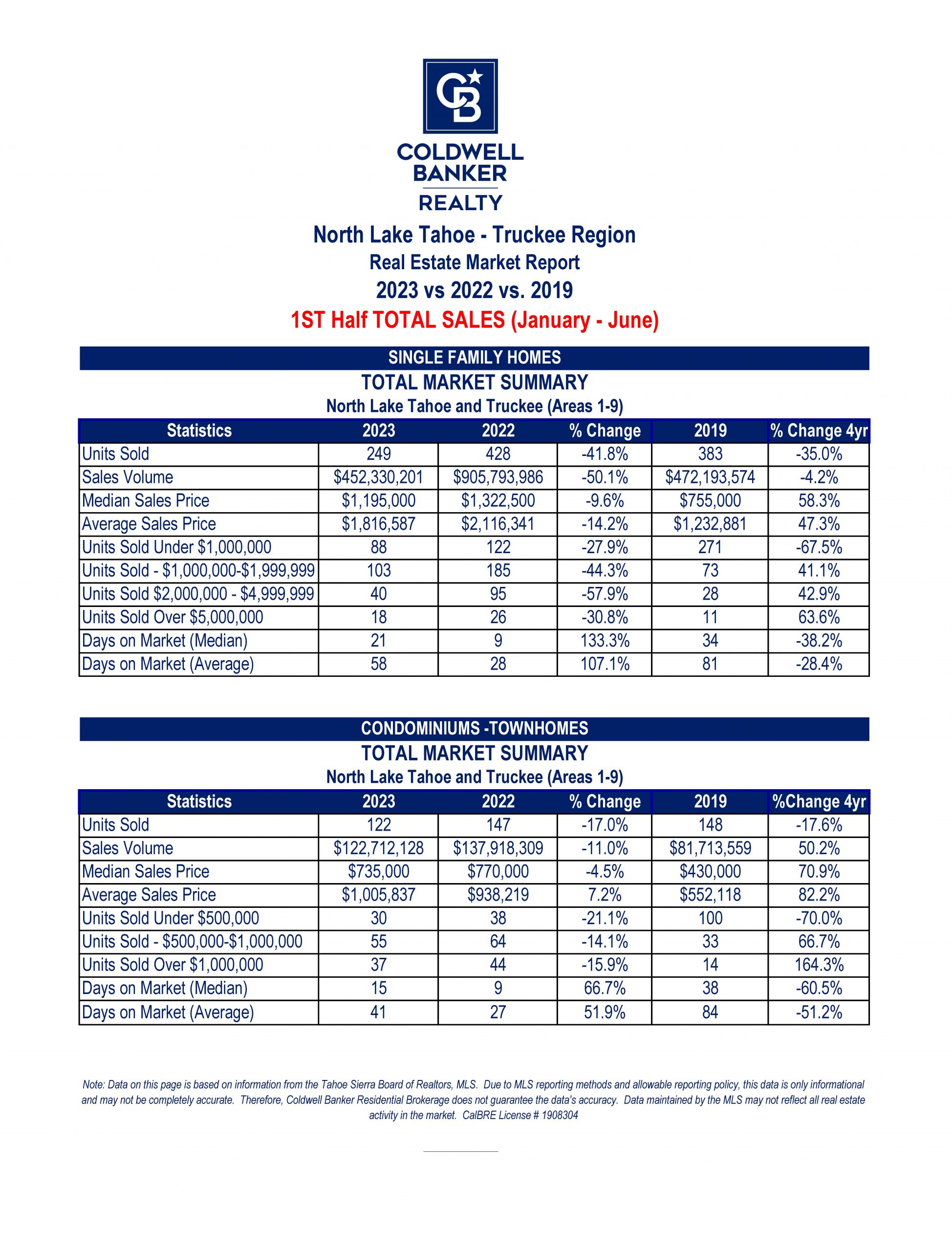

Residential Sales Summary 2023

Total Residential Sales:

Despite what felt like a very quiet market, over half a billion dollars of residential real estate sold in the North Lake Tahoe and Truckee Region in the first half of the year.

In July, 94 residences sold, which is tied for the lowest number of transactions in the last 10 years (July 2014). Ninety four sales is 58% of the 5 year average for the month and 66% of the 10 year average. However, if you remove the 2 COVID “boom” years, the average comes in at 117 transactions and puts this July at 80% of the 10 year average. No matter how you slice it, it was not a highly active month. But, removing the covid years makes it closer to normal.

Through the end of July, 465 residences have sold this year. This marks the lowest 7 month total in the last 10 years and 65% of the 5 year average and 66% of the 10 year average.

Median and Average Sales Prices:

The median sales price for residential real estate in the first half of the year came in at $1.05 million while the average was at $1.5 million.

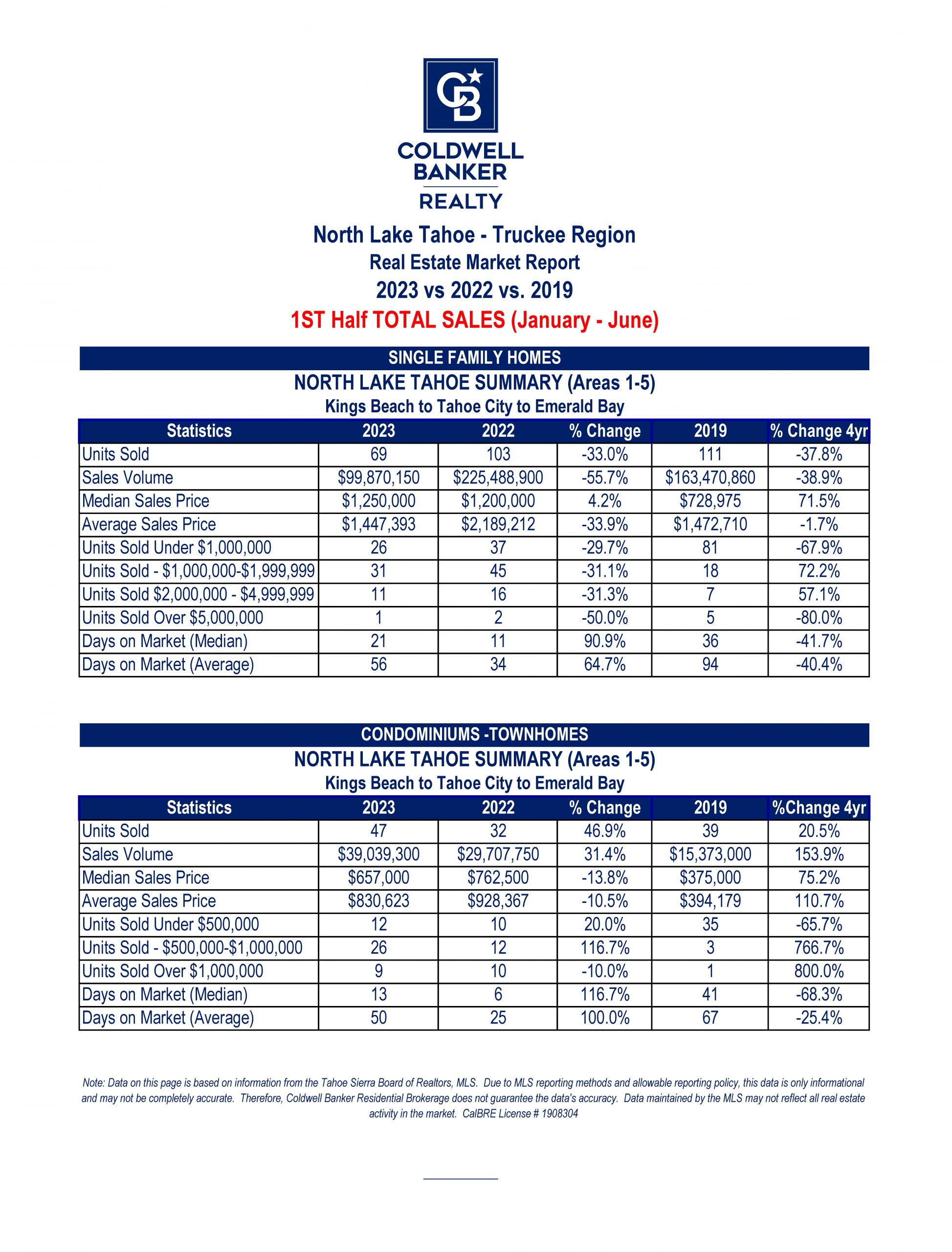

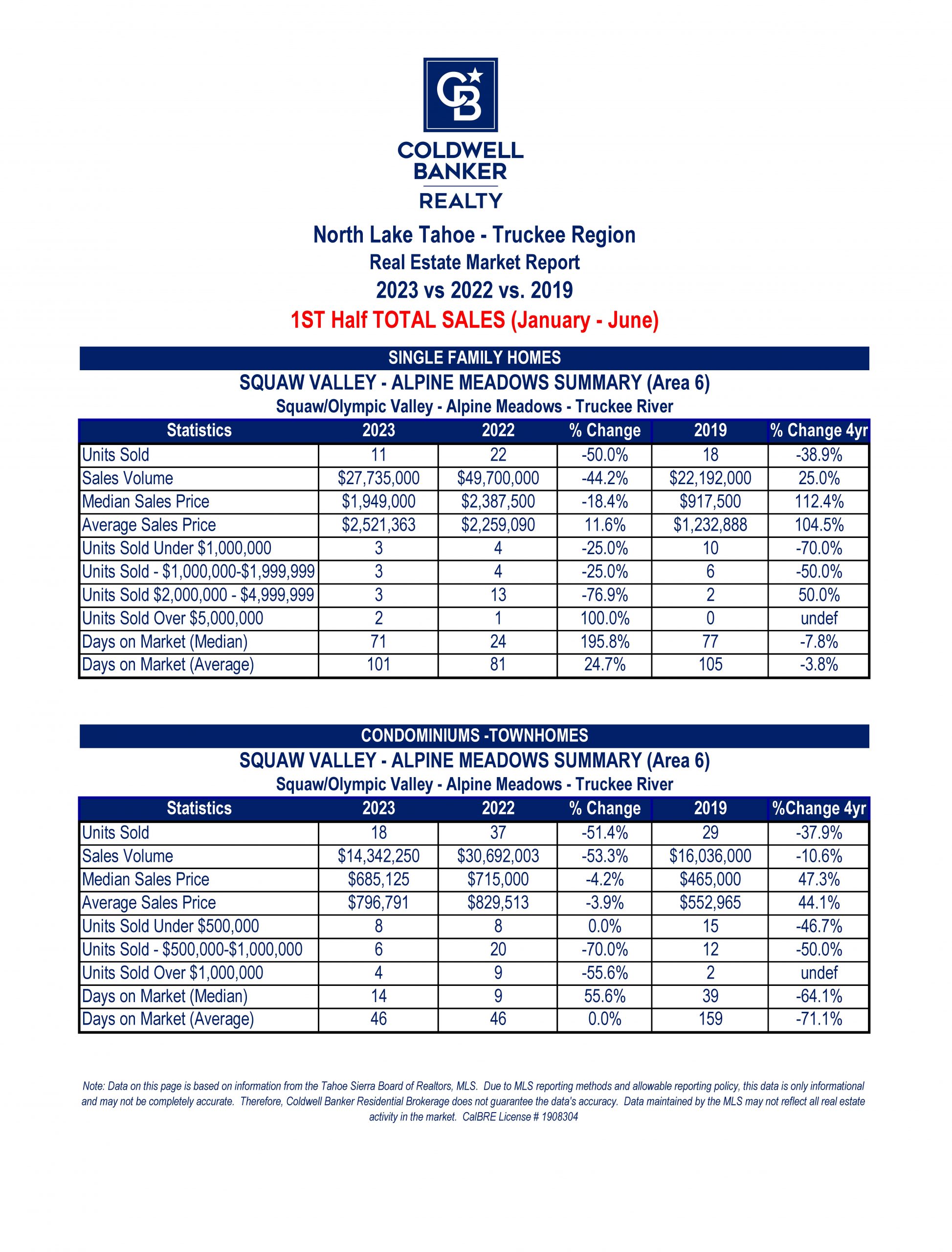

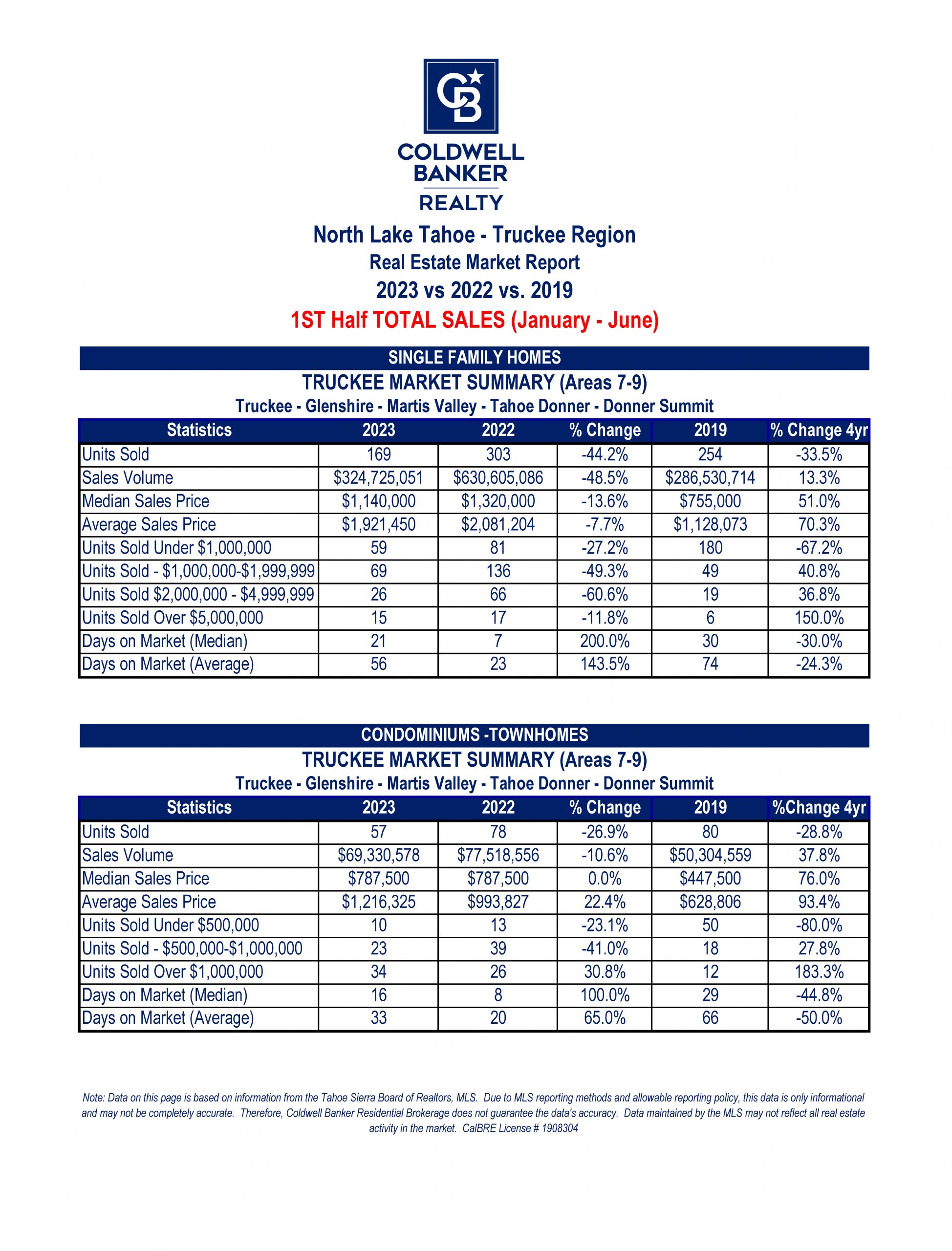

For single family homes only, the median sales price was just below $1.2 million. That represents a decrease of 10% compared to the same period in 2022, but is still 59% higher than the same period in 2019 (pre-pandemic).

For condos, the year to date median was $735,000. That’s down 4.5% compared to the same period in 2022, but up 79% compared to 2019.

So, despite very low numbers of transactions, the strength in pricing gave us the 3rd highest first half sales volume in the last 10 years.

Active Residential Inventory:

Active Listings:

The warm and dry start to summer allowed the snow to melt, and has also given owners ample time to make necessary repairs and put their homes on the market. Active inventory has increased to 350 residences (up from 200 two months ago). Last year, at this time, there were a similar 360 residences actively for sale, but in 2019 the number was closer to 650. Looking at long term numbers, inventory is still at the lowest levels we have seen historically prior to COVID (Around 60% of the average for the 5 years prior to COVID and 40% of the 10 year average) for this time of year.

Current Pending Sales: The number of pending sales is at 140 (after hovering around 60 for the first 4 months of the year). About 140 residences went into contract in July (up significantly from 50-60 the first 4 months).

Current inventory represents about 2.5 months of supply. Historically any number below 5 months of supply is considered a seller’s market. But, this is a much more balanced market, with slight advantages to buyers or sellers in different price ranges.

Sales Under $500,000: January through July there were 19 sales under $500k, representing 10% of all residential sales. For the same period in 2022, 7% of sales were under $500k.

Mid-Range Market Sales $500,000 to $999,999: 75 residences have sold between $500,000 and $999,999, representing 39% of total sales. In 2022, 34% of sales were in this price range.

High End Home Sales $1,000,000 to $1,999,999: 63 residences sold between $1m – $2m, representing 33% of total sales. In 2022, 35% of residential sales were in this range.

Luxury Home Sales Over $2 Million: 34 residences sold over $2 million, representing 18% of sales. This includes 10 sales over $5 million. In 2022, 23% of residential sales were over $2 million including 20 sales over $5 million.

What’s Going On Looking Forward?

Per the Sierra Snow Lab on Donner Summit, this was the 2nd snowiest winter since they started keeping records in 1946. The intense winter definitely impacted what was already a slowing real estate market in the first half of the year. But, winter finally gave way to a beautiful summer with full lakes and rivers!

In the past, big winters have resulted in increased supply in the spring and summer (seller’s saying, “I don’t want to deal with that again”) while also increasing demand (buyer’s saying, “what an incredible ski season, let’s buy a house!”). That seems to be playing out on the demand side, with solid buyer activity resurfacing in June and July. The supply side has not truly surged though. Low inventory continues to be the story with a similar number of active listings to what we saw in summer 2022. That said, inventory was delayed in coming on the market this spring, opening up the possibility that new listings may continue entering the market well into the fall season.

Sellers, keep in mind, this is still a much better time to be a seller than it was in 2019 (which seemed like a very healthy market at the time!). You can expect a similar amount of time on market, but much higher sales prices!

Buyers, keep in mind, this is the most balanced market we have seen in the last 3 years. You now have the following things working in your favor:

- The ability to negotiate price is back!

- The ability to inspect a property and have normal contingencies is back!

- The ability to negotiate repairs is back!

- Yes, interest rates are climbing, but if they continue to climb you will be glad you locked in now. If/when they do reverse course, you can refinance to take advantage!

Contact Me Today to Find Out More about the Opportunities Available in the North Lake Tahoe-Truckee Market.

Note: Data on this page is based on information from the Tahoe Sierra Board of Realtors, MLS. Due to MLS reporting methods and allowable reporting policy, this data is only informational and may not be completely accurate. Therefore, Coldwell Banker Realty does not guarantee the data’s accuracy. Data maintained by the MLS may not reflect all real estate activity in the market. CA-BRE License # 01908304